Retirement plans as a recruiting tool are a proven strategy to attract potential employees that wouldn’t consider working with you otherwise.

GroupRetirement

Affordable Group Retirement Plans for Your Business

Employee Benefits As Low As $.30/hour per Employee

Group Retirement, also referred to as group pensions, is a general term often used to describe any company sponsored savings plan to help employees save for their retirement. Group retirement plans can be very easy to set up and administer, making them a fast growing employee benefit.

The Peace of Mind of Retirement Benefits Helps Attract & Retain Talent

There are many advantages to group retirement or employee pension plans if you’re an employer or the administrator of a qualifying organization.

Retirement plans as a retention tool are a great perk for current valued employees, helping ensure they don’t move to another employer just to get a pension.

Doing the right thing by providing retirement benefits to your employees it can make the difference between them being set for retirement or having to work past their planned retirement age.

Retirement plans create happy employees which improves productivity, means less absenteeism and contributes to higher morale. Healthy and financially secure employees are generally more positive about their place of work and more loyal to their employers.

Group Retirement Plans - Customizing the Right Plan for Your Business

The costs of a Group Retirement Plan for an employer is only based on what the Company contributes to each employee’ account. The cost varies based on a number of factors, including:

The number of employees you have

If the plan is voluntary or mandatory for employees to enroll

The number of employees who sign up for the plan if enrolment is voluntary

The income level of employees

If the plan has an annual cap on the company contribution to an employee’s account

How long employees must work for the Company before they can join the plan

Start Your Free Quote Today

Take advantage of group retirement opportunities

Take advantage of employee benefit opportunities

Hello,

Your questions are important to us at BF Partners. Thank you for your inquiry. One of our Senior Associates will follow up with you by phone and email within the next business day. Please call 1-866-442-2587 if you have any immediate questions.

Best regards,

Paul Bajus

Director Group Retirement

Oops, there was an error sending your message.

Please try again later or call us at 1-866-442-2587. Our apologies for any inconvenience.

Or call 1-866-442-2587 Monday - Friday 9am to 6pm

Group Retirement Plans

at a Glance

We offer different styles of Group Retirement Plans - Basic, Enhanced, and Enhanced+

Basic

A basic plan is an excellent offering for smaller companies who are just starting a plan. Simple, easy to administer and high value for employees

Basic

Protection Plan

Enhanced

An Enhanced plan is better for slightly larger companies, or companies looking to be highly competitive in the war for hiring quality employees. Slightly higher contribution levels and more investment options add value to the plan compared to a Basic Plan.

Enhanced Protection Plan

Enhanced+

Designed to be a highly valued part of an employee’s pay package, an Enhanced+ Plan, fully customizable, sets your offering apart from the competition. An Enhanced+ Plan is frequently used for executive and professional level employees, where a Basic or Enhanced plan may be in place for other employees in the same Company.

Enhanced+ Protection Plan

* Any BFP Group Retirement Plan provides an amazing opportunity for an employer to impact the lives of their employees. Initial and ongoing financial education and retirement planning is part of the benefits of a BFP Group Retirement plan. Employees highly value this education, as well as the enhanced opportunity to save for retirement. Studies have shown that a financially healthy employee is much less stressed, is more productive, and misses less work.

Desirable for Small Business

It pays for Small Business to take advantage of group insurance opportunities.

Affordable – Costs are as low as 2% of payroll, with no other direct costs or fees. Management fees for the investments are almost always much lower than for individual plans.

Manageable

– A group retirement plan is very easy to manage; monthly contributions to the plan are made by a designated administrator at your company in a single lump sum to the plan provider. The plan provider and BFPartners handle all other financial matters.

Shareable

– Employees almost always must contribute to the plan before the company will match, creating a cost sharing arrangement.

Tax Benefits

– A Group Retirement plan creates a tax deduction for both the company and the employee. Compared to a wage increase, the Group Retirement plan will not increase payroll taxes such as EI, CPP and WCB.

Our Client's Say

“Bajus Financial provides Haney Builders Supplies with a group benefit plan with our best interests in mind. Mark Bajus and his team tailored our plan focusing on our budget with low cost options while ensuring we take advantage of new plan options that would provide additional peace of mind to our employees. Our group benefits plan has attracted and retained valuable employees to aid in the success of our business. This approach to service is why I highly recommend the Bajus Financial team for your benefits plan.”

Karl Peters

Controller, Haney Builders Supplies

“Mark spent a great deal of time working out a custom benefit plan solution for us, and it has worked out great. Staff really appreciate that as a small business, we have committed to them with a great benefit plan that’s highly affordable."

Louis Ramos

President, Ramos Holdings Ltd

Attract and Retain Talent

Start your free quote

Hello,

Your questions are important to us at BF Partners. Thank you for your inquiry. One of our Senior Associates will follow up with you by phone and email within the next business day. Please call 1-866-442-2587 if you have any immediate questions.

Best regards,

Paul Bajus

Director Group Retirement

Oops, there was an error sending your message.

Please try again later or call us at 1-866-442-2587. Our apologies for any inconvenience.

Filling out this form will give you a good start on learning the best rates and plans available

Share

Tweet

Share

Mail

Group Retirement

Affordable Group Retirement Plans for Your Business

Group Retirement Plans As Low As $.30/hour per Employee

Group Retirement, also referred to as group pensions, is a general term often used to describe any company sponsored savings plan to help employees save for their retirement. Group retirement plans can be very easy to set up and administer, making them a fast growing employee benefit.

The Peace of Mind of Retirement Benefits Helps Attract & Retain Talent

There are many advantages to group retirement or employee pension plans if you’re an employer or the administrator of a qualifying organization.

Retirement plans as a recruiting tool are a proven strategy to attract potential employees that wouldn’t consider working with you otherwise.

Retirement plans as a retention tool are a great perk for current valued employees, helping ensure they don’t move to another employer just to get a pension.

Doing the right thing by providing retirement benefits to your employees can make the difference between them being set for retirement or having to work past their planned retirement age.

Retirement plans create happy employees which improves productivity, means less absenteeism and contributes to higher morale. Healthy and financially secure employees are generally more positive about their place of work and more loyal to their employers.

Group Retirement Plans - Customizing The Right Plan for Your Business

The costs of a Group Retirement Plan for an employer is only based on what the Company contributes to each employee’ account. The cost varies based on a number of factors, including:

The number of employees you have

If the plan is voluntary or mandatory for employees to enroll

The number of employees who sign up for the plan if enrolment is voluntary

The income level of the employees

If the plan has an annual cap on the compnay contribution to an employee's account

How long employees must work for the Company before they can join the plan

Group Retirement Plans at a Glance

We offer different styles of Group Retirement Plans - Basic, Enhanced and Enhanced+.

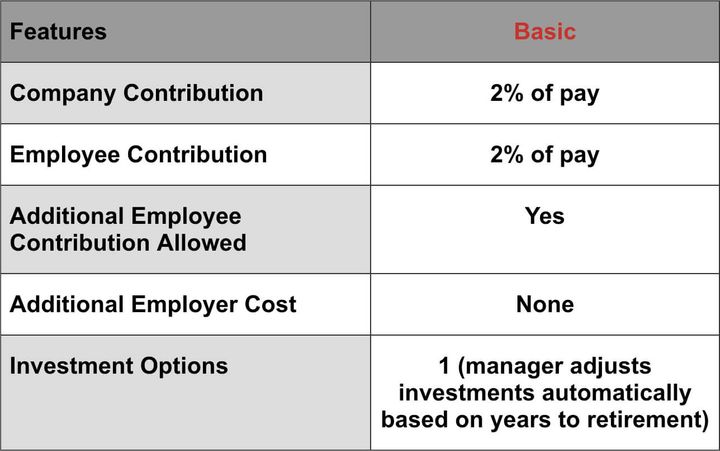

Basic

A Basic plan is an excellent offering for smaller companies who are just starting a plan. Simple, easy to administer and high value for employees

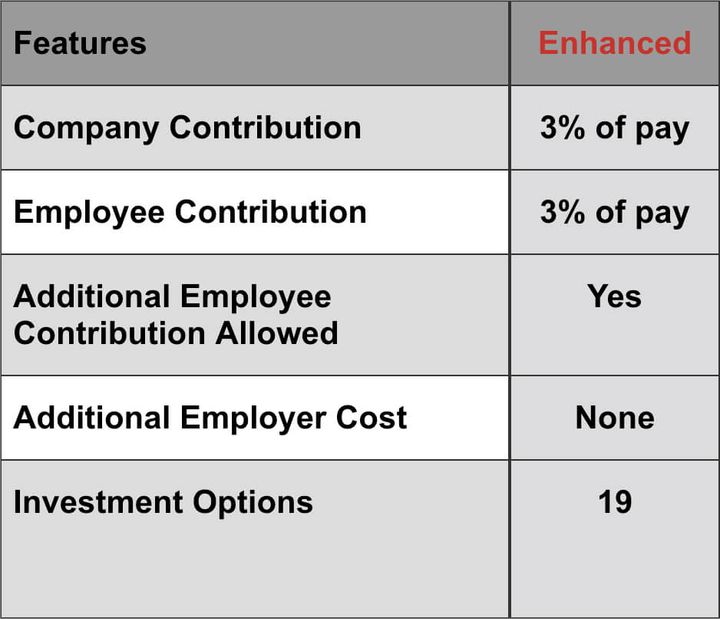

Enhanced

An Enhanced plan is better for slightly larger companies, or companies looking to be highly competitive in the war for hiring quality employees. Slightly higher contribution levels and more investment options add value to the plan compared to a Basic Plan.

Enhanced+

Designed to be a highly valued part of an employee’s pay package, an Enhanced+ Plan, fully customizable, sets your offering apart from the competition. An Enhanced+ Plan is frequently used for executive and professional level employees, where a Basic or Enhanced plan may be in place for other employees in the same Company.

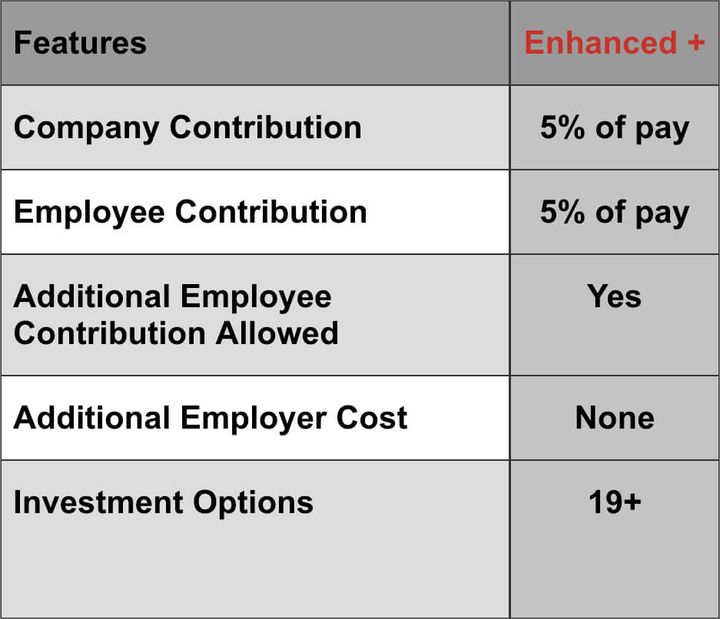

| Features | Basic | Enhanced | Enhanced + |

|---|---|---|---|

| Company Contribution | 2% of pay | 3% of pay | 5% of pay |

| Employee Contribution | 2% of pay | 3% of pay | 5% of pay |

| Additional Employee Contribution Allowed |

Yes | Yes | Yes |

| Additional Employer Cost | None | None | None |

| Investment Options | 1 (manager adjusts investments automatically based on years to retirement) |

19 | 19+ |

| Features | Basic | Enhanced | Enhanced + |

|---|---|---|---|

| Company Contribution | 2% of pay | 3% of pay | 5% of pay |

| Employee Contribution | 2% of pay | 3% of pay | 5% of pay |

| Additional Employee Contribution Allowed |

Yes | Yes | Yes |

| Additional Employer Cost | None | None | None |

| Investment Options | 1 (manager adjusts investments automatically based on years to retirement) |

19 | 19+ |

* Any BFP Group Retirement Plan provides an amazing opportunity for an employer to impact the lives of their employees. Initial and ongoing financial education and retirement planning is part of the benefits of a BFP Group Retirement plan. Employees highly value this education, as well as the enhanced opportunity to save for retirement. Studies have shown that a financially healthy employee is much less stressed, is more productive, and misses less work.

Start Your Free Quote Today

Take advantage of group retirement opportunities

Take advantage of employee benefit opportunities

Hello,

Your questions are important to us at BF Partners. Thank you for your inquiry. One of our Senior Associates will follow up with you by phone and email within the next business day. Please call 1-866-442-2587 if you have any immediate questions.

Best regards,

Paul Bajus

Director Group Retirement

Oops, there was an error sending your message.

Please try again later or call us at 1-866-442-2587. Our apologies for any inconvenience.

Or call 1-866-442-2587 Monday - Friday 9am to 6pm

Share

Tweet

Share

Mail

Attract and Retain Talent

Start your free quote

Hello,

Your questions are important to us at BF Partners. Thank you for your inquiry. One of our Senior Associates will follow up with you by phone and email within the next business day. Please call 1-866-442-2587 if you have any immediate questions.

Best regards,

Paul Bajus

Director Group Retirement

Oops, there was an error sending your message.

Please try again later or call us at 1-866-442-2587. Our apologies for any inconvenience.

Filling out this form will give you a good start on learning the best rates and plans available

Filling out this form will give you a good start on learning the best rates and plans available

Desirable for Small Business

It pays for Small Business to take advantage of group insurance opportunities.

Affordable – Costs are as low as 2% of payroll, with no other direct costs or fees. Management fees for the investments are almost always much lower than for individual plans.

Manageable

– A group retirement plan is very easy to manage; monthly contributions to the plan are made by a designated administrator at your company in a single lump sum to the plan provider. The plan provider and BFPartners handle all other financial matters.

Shareable

– Employees almost always must contribute to the plan before the company will match, creating a cost sharing arrangement.

Tax Benefits

– A Group Retirement plan creates a tax deduction for both the company and the employee. Compared to a wage increase, the Group Retirement plan will not increase payroll taxes such as EI, CPP and WCB.

Benefits and Pensions Blogs

Our Client's Say

“Bajus Financial provides Haney Builders Supplies with a group benefit plan with our best interests in mind. Mark Bajus and his team tailored our plan focusing on our budget with low cost options while ensuring we take advantage of new plan options that would provide additional peace of mind to our employees. Our group benefits plan has attracted and retained valuable employees to aid in the success of our business. This approach to service is why I highly recommend the Bajus Financial team for your benefits plan.”

Karl Peters

Controller, Haney Builders Supplies

“Mark spent a great deal of time working out a custom benefit plan solution for us, and it has worked out great. Staff really appreciate that as a small business, we have committed to them with a great benefit plan that’s highly affordable."

Louis Ramos

President, Ramos Holdings Ltd